Property Investment Strategy Australia: How Property Investing Actually Creates Wealth

Most Australians understand that property builds wealth over time. Fewer understand why some investors compound that wealth across multiple properties while others stall after the first purchase.

This is especially true for property investment in Australia in the current 2026 environment.

The difference is rarely luck or timing. It is strategy. In 2026, tighter lending conditions, compressed borrowing power, and shifting rental dynamics have made the choice of property investment strategy in Australia more consequential than at any point in the past decade. This article explains how the main strategies actually work, which ones suit which investor profiles, and what experienced investors do differently.

For investors focused on building wealth through property, understanding strategy is now more important than simply entering the market.

Why Strategy Selection Has Changed in 2026

For most of the past two decades, Australian property investors operated in an environment where almost any strategy produced acceptable results. Low interest rates, loose credit conditions, and sustained price growth across major capitals meant that execution mattered less than simply getting into the market.

That environment no longer exists. The APRA serviceability buffer sits at 3% above the lending rate, which means a loan assessed at 9.5% today is being stress tested against repayments that would have seemed extreme even three years ago. Borrowing power for the average investor has contracted by 20 to 30% compared to the 2021 cycle peak.

In this environment, a poorly chosen strategy does not just underperform. It can consume the borrowing capacity that a better strategy would have used to acquire a second or third property.

The Core Property Investment Strategies Explained

There are more strategy names in Australian property investing than there are genuinely distinct approaches. Most reduce to a handful of fundamental methods, each with a different risk profile, capital requirement, and portfolio fit.

All effective strategies start with a strong grasp of supply and demand fundamentals in the target market.

Buy and hold is the foundation of most successful Australian portfolios. The investor acquires a property in a market with strong underlying demand, holds it through market cycles, and compounds equity over time. It requires patience and serviceability but carries lower execution risk than active strategies.

Positive gearing targets properties where rental income exceeds all holding costs. These assets are typically found in regional markets or at lower price points. The trade-off is that strongly cash flow positive properties frequently offer lower capital growth trajectories.

Negative gearing involves holding a property where costs exceed rental income, with the shortfall offset against other taxable income. It has historically suited high-income investors in capital city growth markets. In a higher rate environment the holding cost increases significantly, which compresses the strategy's effectiveness.

Rentvesting involves renting in a preferred location while buying an investment property in a more affordable or higher yield market. It has grown substantially as an entry strategy as capital city prices have moved beyond the reach of many first-time investors.

Strategy Comparison: Risk, Growth and Cash Flow

Buy and hold delivers the strongest long term capital growth of the core strategies. Positive gearing leads on cash flow but typically trades off growth potential in exchange.

Source: FPW Group strategy analysis; CoreLogic historical return data, 2025 to 2026.

Capital Growth vs Rental Yield: Which Matters More Now

The growth versus yield debate has been a fixture of Australian property investing for decades. In the current environment, the answer is more nuanced than it has ever been.

Capital growth compounds wealth over time and underpins the equity recycling that allows experienced investors to fund subsequent acquisitions without additional cash savings. A $600,000 property that grows at 6% annually adds $36,000 in equity in the first year. That equity, accessed through a refinance, can partially fund the next deposit.

Rental yield, by contrast, affects cash flow and therefore serviceability. In an environment where every dollar of rental income strengthens the next loan application, yield has become a more strategic variable than it was during the low-rate cycle.

For Example

An investor holding two properties with an average yield of 3.5% will have a meaningfully weaker serviceability position when applying for a third loan than an investor holding two properties yielding 5.2%. The lender counts 75 to 80% of rental income toward serviceability. At scale, that difference can determine whether a third acquisition is possible at all.

Capital Growth vs Yield Trade Off Across Market Types

Inner city capital markets deliver stronger long run growth but significantly lower yields. Regional markets reverse that dynamic and are increasingly relevant for investors managing serviceability constraints.

Source: CoreLogic; RBA; FPW Group modelled analysis, 2025 to 2026.

How Lending Conditions Shape Strategy Viability

What investors often discover too late is that their strategy choice and their borrowing structure are not independent decisions. They interact at every stage of a growing portfolio.

This is closely tied to how interest rates affect investment strategy, especially in the current higher-rate environment.

An investor pursuing a pure capital growth strategy in an inner-city market will typically accept a lower yield. That lower yield reduces the rental income counted toward serviceability. Over multiple properties, the cumulative effect can bring a portfolio to a halt well before the investor intended.

The investors who continue acquiring past property two or three are almost always those who factored lending sequencing into their strategy from the beginning and not as an afterthought.

Rentvesting and Alternative Entry Strategies

Rentvesting has shifted from a niche workaround to a mainstream entry strategy for a reason. In markets where median prices sit well above $1 million, the traditional path of buying a home first and investing second can delay investment entry by years while the investor waits to accumulate a larger deposit.

By renting in their preferred location and buying an investment property in a more accessible market, rentvestors gain earlier market entry, potential tax deductions on the investment property, and exposure to rental yield from day one.

For Example

A Sydney professional renting in Surry Hills for $700 per week purchases a $480,000 investment property in regional Queensland yielding 5.8%. The investment property generates approximately $537 per week in gross rental income.

The investor is in the market, building equity, and receiving rental income that partially offsets their own rent. The tax treatment on the investment property provides additional benefit at tax time.

How Experienced Investors Build Portfolios Over Time

What separates investors who build portfolios of five or more properties from those who stall after the first is rarely income. It is sequencing. The way each acquisition is structured affects the one that follows.

Experienced investors think about each property in terms of what it does to their overall serviceability position, not just what it costs to hold in isolation. A property that costs $200 per week to hold but generates $80,000 in equity over three years provides a refinanceable asset that can fund the next deposit without additional cash savings.

A key part of this is increasing borrowing capacity for future purchases through smart equity recycling.

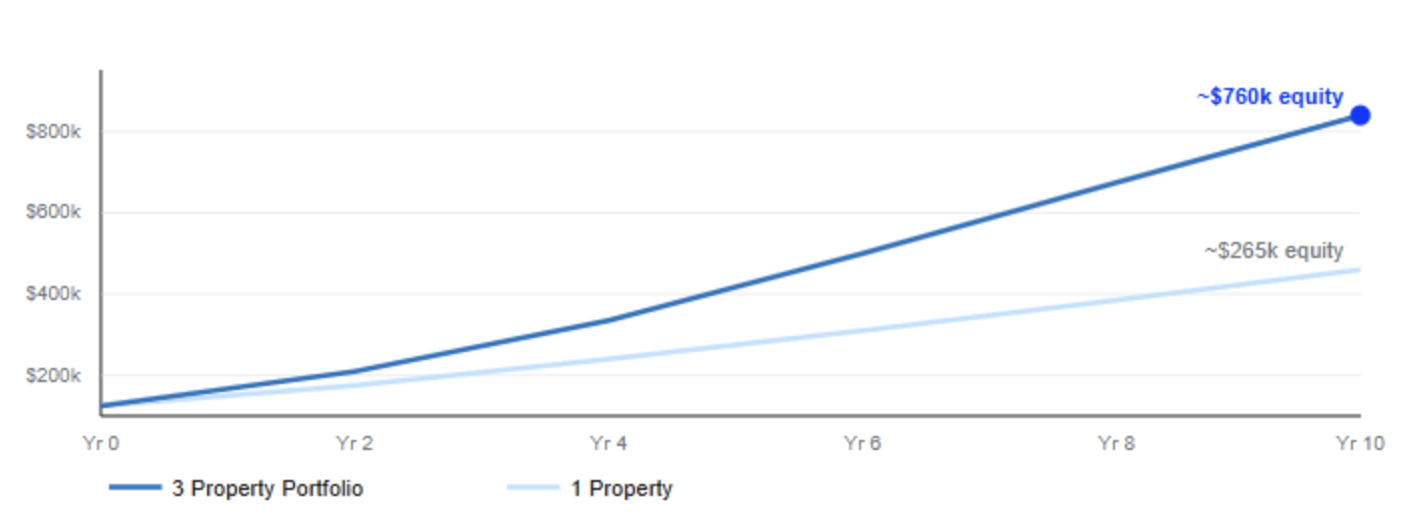

Indicative Portfolio Equity Growth Over 10 Years

A sequenced three property portfolio compounds equity substantially faster than a single property held over the same period, assuming consistent market conditions and deliberate financing structure.

Source: FPW Group modelled scenario; CoreLogic capital growth assumptions at 5.5% p.a., 2025 to 2026. Modelled only. Not a forecast.

Final Thoughts: Choosing the Right Property Investment Strategy

There is no universally correct Australian property investment strategy. There is only the strategy that fits the investor's financial position, risk tolerance, timeline, and borrowing capacity at a given point in time.

Success also depends heavily on choosing the right time to invest based on your personal financial position.

What the 2026 environment has clarified is that strategy selection is no longer optional. When credit was easy and prices were rising everywhere, the strategy mattered less than the decision to act. Today, a poorly matched strategy consumes finite borrowing capacity that a better matched one would have preserved for future acquisitions.

Ready to map a realistic property investment strategy against your current financial position? A strategy session with the FPW Group team covers borrowing capacity, market selection, and acquisition sequence from the first property to the third.

Frequently Asked Questions

Recommended Reading

Two pages selected based on what readers of this article are most likely to need next.