FPW Group · Education Hub

Property Investment Australia: How to Build Wealth Through Real Estate

Property investment in Australia still attracts people who want long-term wealth, but the calculation has changed. Prices are higher, lending tests are tighter, and the margin for poor planning is smaller than it was during the low-rate years. That does not make property investment unworkable. It makes the strategy more important.

In a Nutshell - If you only remember a few things:

Leverage is what makes property powerful. A 10 per cent price rise can produce a 50 per cent return on the cash invested.

Capital growth, not rental yield, drives most long-run wealth creation in Australian residential property.

Holding costs are often higher than investors expect. Management, maintenance, vacancy, insurance, and rates all matter.

Tax benefits can improve the return, but they should never justify a weak investment.

Stage of life determines strategy. A good purchase at 32 may be the wrong purchase at 52.

Financing is now a core constraint. Investors need to plan borrowing capacity before they plan the next acquisition.

Time in the market usually matters more than perfect entry timing.

Table of contents

Table of contents

What is property investment in australia?

Property investment means buying real estate to generate a financial return. That return usually comes from capital growth, rental income, or a combination of both.

It is different from buying a home to live in. The decision should not be based on personal taste, emotional comfort, or whether the investor likes the suburb. It should be based on the asset, the market, the cash flow, the debt structure, and the time horizon.

The Australian Taxation Office reported that more than 2.2 million Australians declared rental income or losses in the 2021 to 2022 financial year. That places investment property beside superannuation as one of the main wealth-building tools used by Australian households.

The model is simple. The discipline required to execute it is not.

An investor buys a property, rental income offsets part of the holding cost, and the asset hopefully appreciates over time. The feature that makes this model powerful is leverage. Most investors do not pay the full purchase price in cash. They contribute a deposit and borrow the rest. That is where the returns become asymmetric.

2.2M+

Australians declared rental income

in FY 2021–22 (ATO)

20%

Standard deposit to avoid Lenders

Mortgage Insurance

50%

Return on a $120k deposit when a

$600k property grows 10%

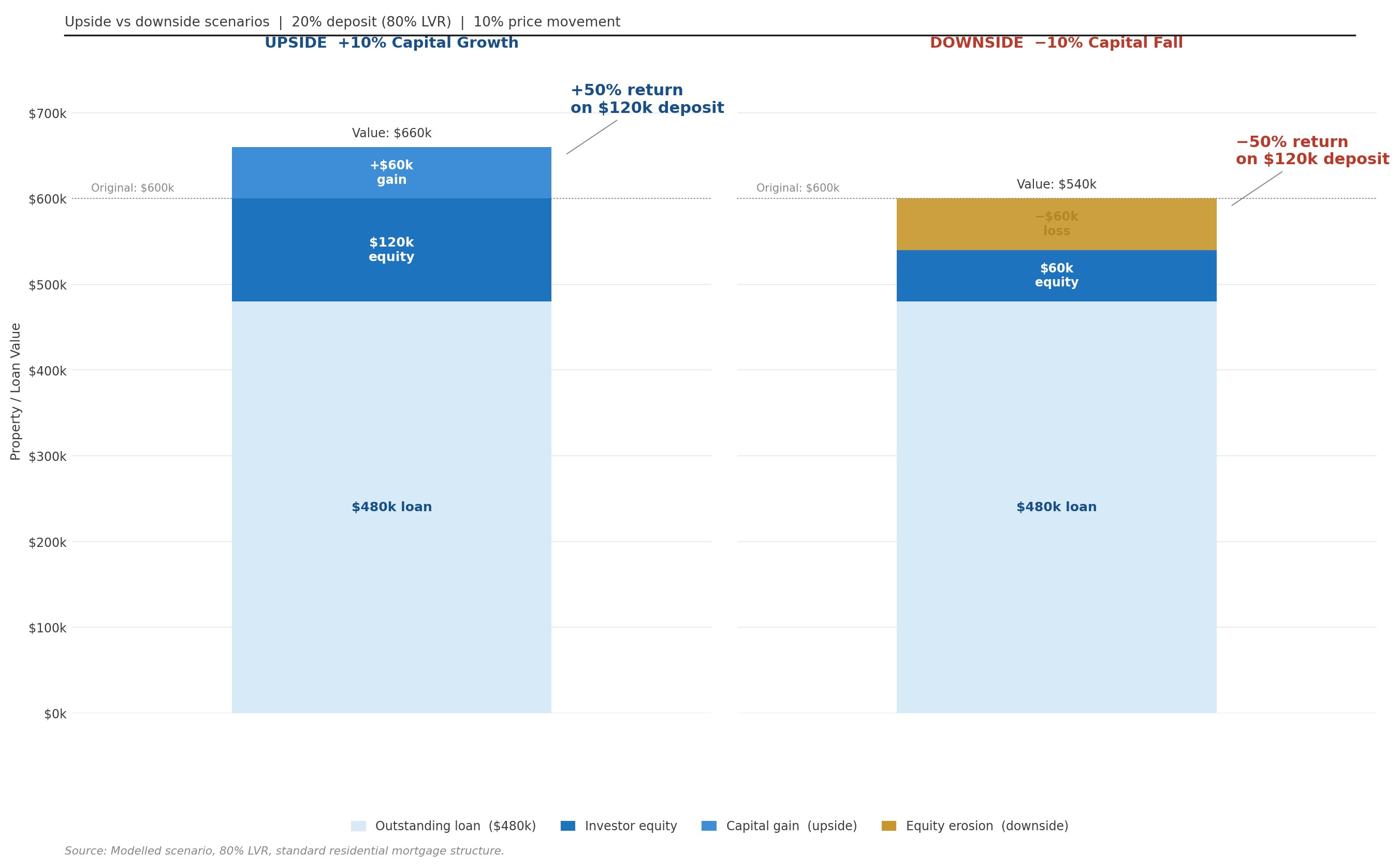

The Leverage Effect: How a $120,000 Deposit Can Control a $600,000 Asset

A 10 per cent price movement has an outsized effect on the investor's actual cash. The upside scenario doubles the equity position, but the same maths works in reverse on a fall — making leverage a tool that demands stress-testing before use, not after.

Source: Modelled scenario, 80 per cent loan-to-value ratio, standard residential mortgage structure.

A 10 per cent increase in value on a $600,000 property produces a $60,000 gain. If the investor contributed a $120,000 deposit, that is a 50 per cent return on the cash invested before transaction costs and tax. The same effect works in reverse when prices fall, so leverage should be stress-tested before the purchase, not explained after the portfolio is under pressure.

A practical example shows why this matters. A buyer who purchased a $550,000 townhouse in Brisbane in 2018 with a $110,000 deposit may have seen that property rise to roughly $820,000 by 2024, based on the direction of CoreLogic’s Brisbane index. The mortgage balance did not create the equity. The market movement did.

That is the attraction of property investment. It allows ordinary households to control a large asset with a smaller amount of cash.

It also explains the risk. Leverage does not only magnify good outcomes.

"Property investment in Australia is not mainly an income strategy. It is a wealth accumulation strategy where leverage and time do much of the work, provided the investor can stay in the position long enough."

What This Means in Practice

A property investor does not need the full purchase price to benefit from capital growth. A 20% deposit gives exposure to the full value of the asset. That is useful, but it is not free. If prices fall, the same leverage amplifies the loss on the investor's equity.

The right question is not only whether the property's value increases, but whether the investor can financially survive the downturns and holding costs along the way without being forced to sell early.

Why australians invest in property

Australians invest in property for cultural reasons, tax reasons, and behavioural reasons. The asset feels familiar. The rules are widely understood. The mortgage creates discipline.

That combination is powerful.

Familiarity and Tangibility

Most Australians first understand property through the family home. They can see it, inspect it, compare it, and form a view on its value. That makes property feel more accessible than shares, funds, or more complex investment structures.

This comfort matters. A multi-decade investment requires confidence, especially when interest rates rise, tenants change, or market commentary turns negative.

The danger is that familiarity can look like knowledge. A suburb an investor likes is not always a suburb with strong investment fundamentals.

The Tax Framework

Australia’s tax rules have influenced how people invest in property. In the past, investors could use negative gearing to reduce their tax by claiming rental losses against their income. They could also receive a 50 per cent discount on capital gains tax if they sold the property after owning it for more than a year.

However, under the new investment rules implemented recently, these benefits would be reduced for many new investors, especially those buying existing properties instead of new homes.

These tax benefits can improve returns, but they do not automatically make a property a good investment.

For example, imagine a nurse earning $95,000 a year who buys a $650,000 investment property with a $500,000 loan at 6.2 per cent interest. The yearly interest cost is about $31,000. If the property earns $24,000 in rent each year, the investor loses about $7,000 before other costs are included.

Under the new system, the investor may receive less tax relief than before. Future profits from selling the property may also be taxed more heavily.

This means investors must focus even more on whether the property itself is likely to grow in value and produce reliable rental income over time.

Tax benefits can help increase returns, but they should not be the main reason for buying an investment property.

The Mortgage as Forced Saving

The mortgage also changes behaviour. It forces regular repayments that many investors would not otherwise make into a savings or investment account.

This is one of the least discussed benefits of property. A household can hold a property for 15 years and accumulate equity partly because the debt structure forced discipline. The result may look like investment brilliance. In practice, it is often a mix of leverage, time, and compulsory saving.

This trend also explains why Australians are becoming accidental investors and the rise of accidental investor trends in Australia.

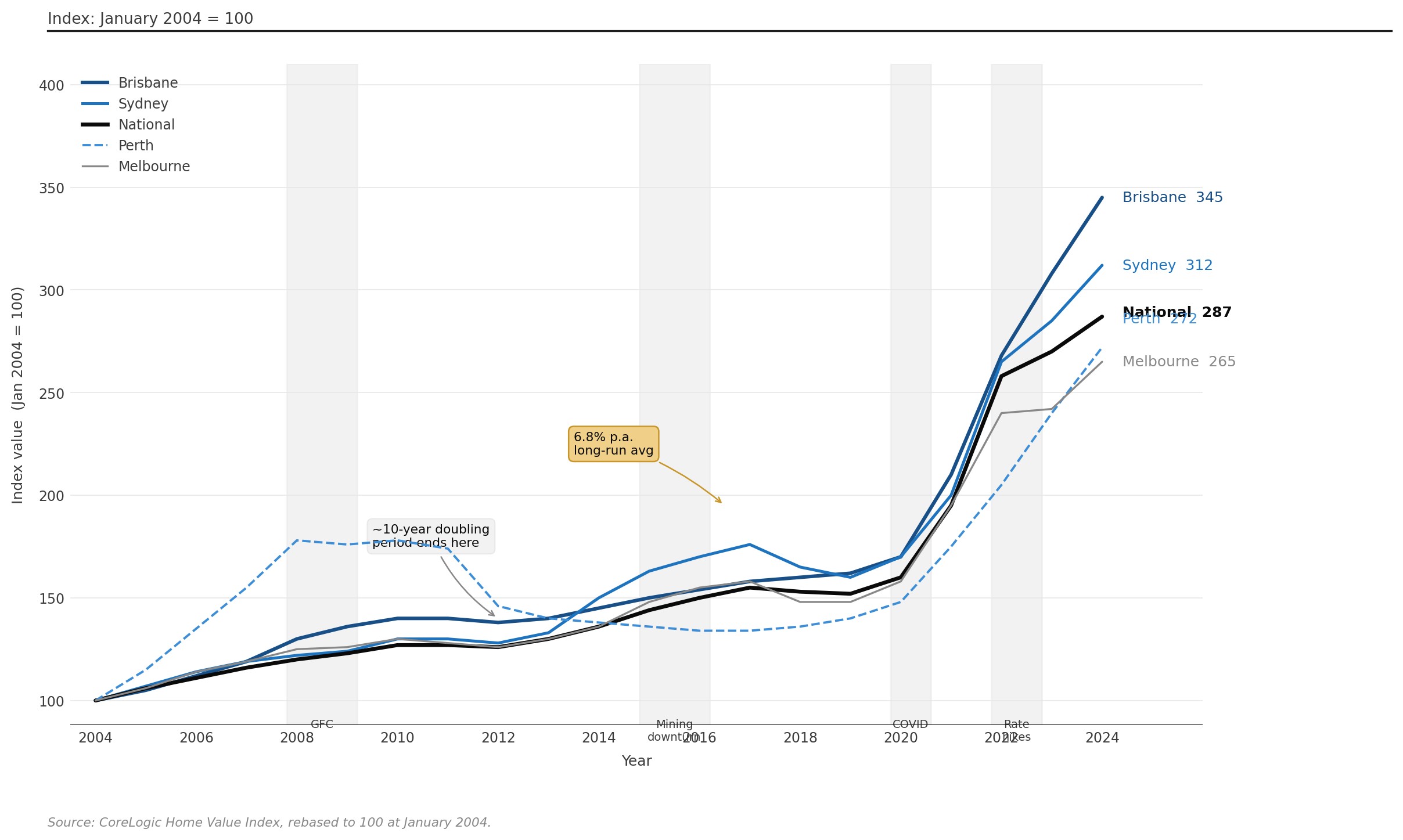

National Dwelling Values, Australia, 2004 to 2024

Brisbane and Sydney have more than tripled in index value since 2004, while Melbourne has broadly tracked the national average. The chart also shows that every city experienced at least one extended flat period — reinforcing why a ten-year minimum horizon changes how entry conditions should be judged.

Source: CoreLogic Home Value Index, national series rebased to 100 at January 2004.

CoreLogic’s long-run dwelling value data shows why property remains central to household wealth in Australia. The national average can hide weak local markets and flat periods, but quality assets held through full cycles have historically rewarded patience more than short-term timing.

Investors who bought at periods described as expensive, including 2004, 2010, and 2017, often saw those assets appreciate meaningfully over the following decade. That does not guarantee the same result for future buyers. It does show why a ten-year holding period changes the way entry conditions should be judged.

Australians also closely monitor long-term housing demand trends when making investment decisions.

“The question is not whether the market feels expensive on the day of purchase. The better question is whether the asset is strong enough to justify being held through a full cycle.”

What This Means in Practice

Tax benefits and long-run market growth can help an investor, but neither replaces asset selection. A weak property with a tax deduction is still a weak property.

The stronger approach is to buy an asset with sound fundamentals, then use tax settings and financing structure to improve the holding position.

How property investment works

Property investment works through four main return drivers: capital growth, rental income, tax efficiency, and equity recycling. The order matters.

For most Australian residential investors, capital growth does most of the heavy lifting. Rental income helps carry the asset, but it usually does not create the main wealth outcome.

Capital Growth: The Primary Wealth Driver

Capital growth is the increase in market value over time. If a $700,000 property grows at 6 per cent per year, it may be worth about $940,000 after five years, before costs and tax.

The owner does not need to renovate, trade frequently, or make daily decisions to create that uplift. The return comes from owning a good asset in a market where demand, supply, income, infrastructure, and credit conditions support value growth.

That sounds passive. However, it is not that simple.

The difficult work happens before purchase: selecting the right market, avoiding weak assets, and making sure the cash flow is sustainable.

Rental Income: Useful, but Often Overestimated

Rental income helps offset mortgage interest, rates, insurance, repairs, management fees, and vacancy. In some markets, rent can cover a large share of the holding cost. In Sydney and Melbourne, many investors accept a shortfall because they expect stronger long-term growth.

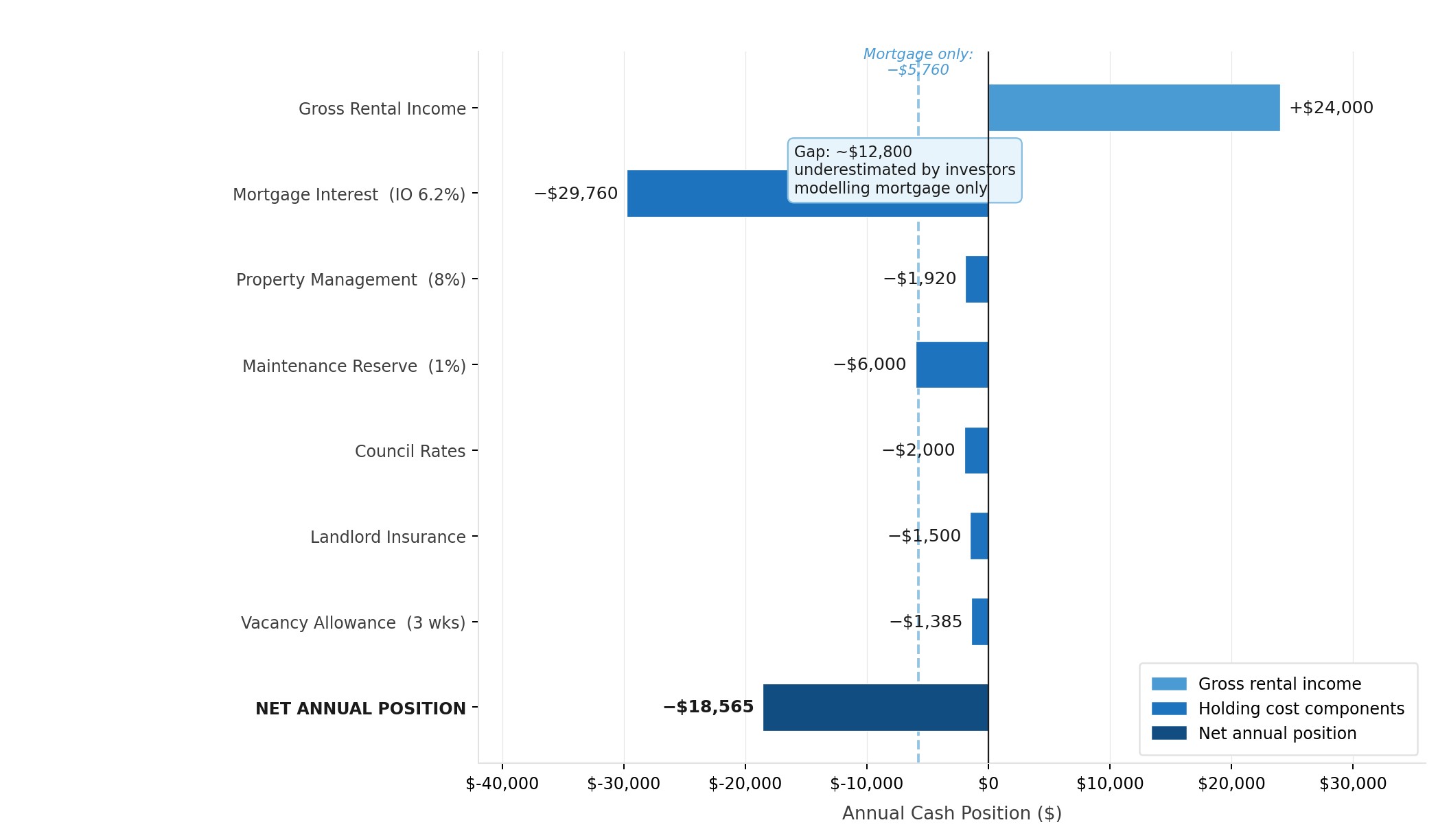

Where investors usually misread this is the gap between gross rent and net rent. A $600,000 property earning $24,000 in gross rent does not put $24,000 in the investor’s pocket.

That profit would even look close to neutral if the investor compares rent only with mortgage interest. Once property management, maintenance, council rates, insurance, and vacancy are included, the position can move materially negative. This is where investors discover whether the portfolio is genuinely manageable or only looked manageable in a spreadsheet.

Successful investors understand Australia’s housing shortage explained and why housing supply matters to investors. They also regularly check market indicators investors should watch.

The gap between gross rent and true net position is typically $10,000–$15,000 wider than investors model at purchase. Mortgage interest dominates, but the smaller line items, management, maintenance, vacancy, compound into a material shortfall that only becomes visible once the property is held for a full year.

Source: Modelled scenario using management fees, maintenance, insurance, rates, and vacancy assumptions.

The real cost of property management is often underestimated because it feels small as a percentage. The problem is not the individual cost. It is the combined effect of several small costs arriving every year.

Tax Efficiency: Helpful, Not Foundational

Depreciation, deductible interest, and other investment property tax deductions can improve after-tax outcomes. Newer properties may also generate stronger depreciation benefits in the early years.

This can be meaningful for higher-income investors. It can reduce the cash cost of holding the asset while the investor waits for capital growth.

But the logic must stay in the right order. The property should make sense first. Tax should improve the outcome second.

Equity Recycling: How Portfolios Expand

Equity recycling is how many investors move from one property to two, then potentially to a broader portfolio. As the property rises in value and the loan reduces, the investor may be able to access part of the equity to fund another deposit.

A buyer who purchased in Adelaide in 2019 for $480,000 may now hold enough usable equity to support a second acquisition, depending on lender policy, income, and serviceability.

This is where the system becomes more complex. Equity can solve the deposit problem, but income still needs to satisfy the lender.

A portfolio can become wealthier on paper while becoming harder to scale.

“Equity recycling is not a loophole. It is the mechanism that turns one successful property into the funding base for the next, provided the investor still has the income to service the debt.”

What This Means in Practice

Model the full holding cost before you buy. Include management fees, maintenance, vacancy, insurance, rates, and a higher-rate scenario.

A property that appears neutral at first glance may still require thousands of dollars a year in support. That does not make it a bad investment. It means the investor needs to know the carrying cost before the contract is signed.

Property investment strategies

Not every investor should pursue the same approach. The right strategy depends on income, life stage, risk tolerance, and timeline. Property investment strategies for Australians and approaches to building a property portfolio vary depending on your goals and life stage. The four core approaches each have a different emphasis.

Capital Growth Strategy

The capital growth strategy prioritises long-term appreciation over current income. The investor accepts negative or near-neutral cash flow in exchange for exposure to high-growth markets, typically inner and middle ring metropolitan areas with strong land value, employment density, and infrastructure investment.

This approach suits younger investors with time ahead of them and income to support holding costs through rate cycles. It is less suitable for investors approaching retirement who need their portfolio to generate income.

Cash Flow Strategy

The cash flow strategy prioritises rental yield, with the goal of owning properties that generate more income than they cost to hold. This approach is common in regional markets and smaller cities where yields are higher relative to purchase prices.

The trade-off is growth. Many high-yield markets have weaker historical appreciation. Cash flow investors often build portfolios that generate income but do not accumulate the same equity as growth-focused investors over 20 years. The approach can work well as part of a blended portfolio, or for investors in the income and retirement stage.

Balanced Strategy

A balanced strategy attempts to combine reasonable growth potential with acceptable cash flow. The goal is an asset that does not require heavy monthly support while still sitting in a market with solid long-run appreciation drivers.

This is often the most practical approach for investors in their 40s managing multiple priorities. It avoids the extremes of pure growth assets that drain cash flow and pure yield assets that may never build meaningful equity.

Portfolio Growth Strategy

A portfolio growth strategy focuses on sequencing acquisitions to maximise future borrowing capacity. Each purchase is evaluated not only on its own return, but on how it affects the next move.

This approach requires more planning and usually involves working with a finance specialist alongside a buyers agent or property adviser. The goal is to build a portfolio of three to five well-positioned assets over a ten to fifteen year period, with each acquisition strengthening rather than limiting the ones that follow.

Before Buying Any Investment Property, Ask:

Does it align with my stated investment objective?

Does it improve or limit my future borrowing capacity?

Can I comfortably hold it through adverse conditions, including rate rises and vacancy?

Does this asset strengthen the overall portfolio, or does it add concentration risk?

Can you still afford an investment property in australia?

Affordability is the question many first-time investors ask first. In 2026, it is a fair question.

Median prices in Sydney, Brisbane, and Adelaide have risen materially since the pandemic period. Interest rates also remain much higher than the emergency settings of 2020 and 2021. Even where prices stabilise, borrowing capacity may still limit what an investor can buy.

Popular choices include best cities for property investment such as Brisbane, Adelaide, and Perth.

The constraint is no longer prices alone. It is financing mechanics.

Price and Borrowing Power Are Separate Problems

A lower purchase price does not always make a property easier to hold. A cheaper asset with weak rental demand, poor growth prospects, or high maintenance can still damage a portfolio.

At the same time, a strong asset can be unaffordable if the debt required exceeds what the investor can service under lender assessment rules.

That is why affordability should be split into two questions:

Can I buy the property?

Can I hold the property through a range of conditions?

Those are not the same question.

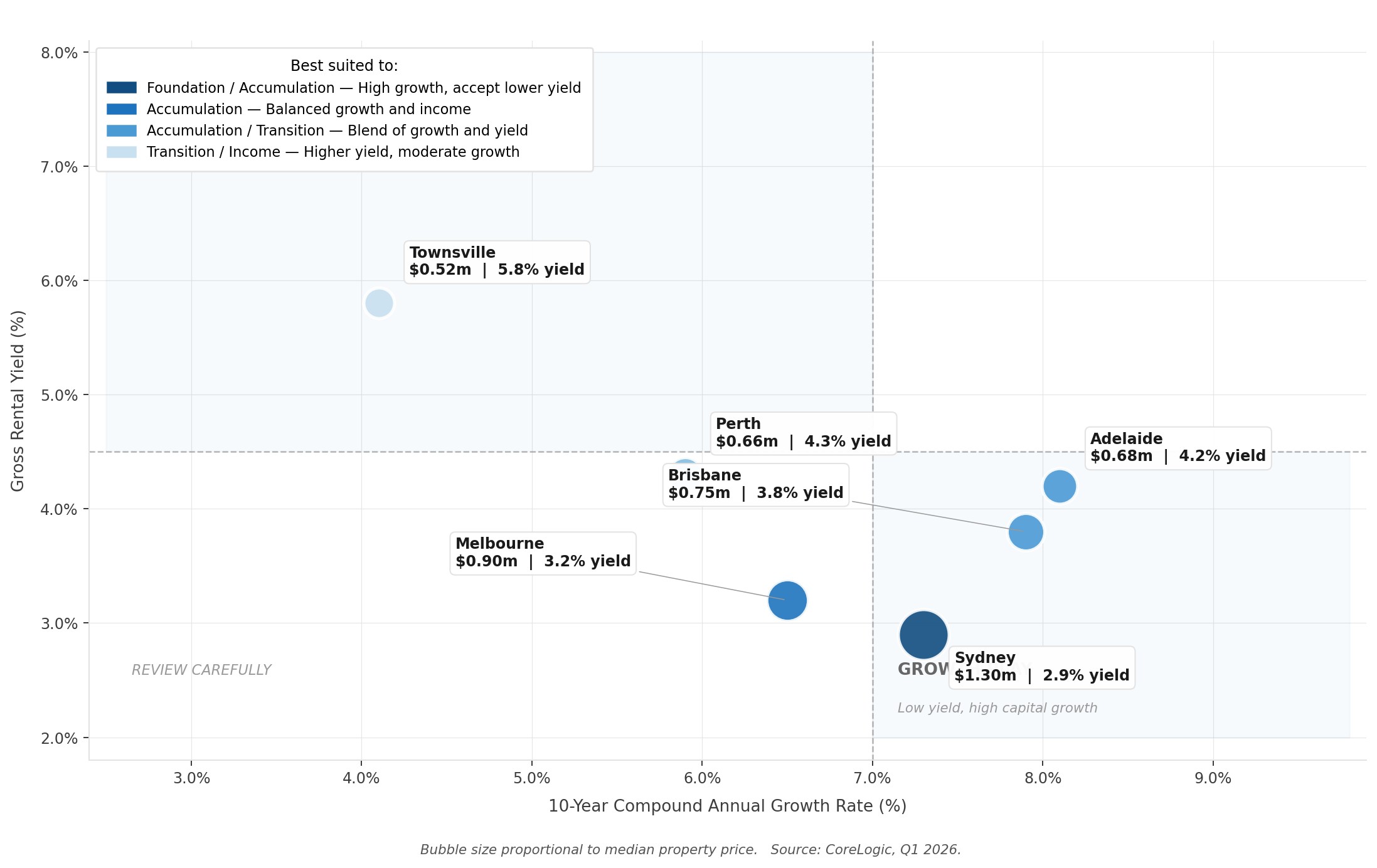

No single market dominates across both dimensions. Sydney offers the strongest long-run growth case but the weakest yield, while Townsville sits in the opposite corner. Investors choosing between markets are ultimately choosing between a cash flow burden now and a potential equity reward later.

Source: CoreLogic median values and yield data, Q1 2026. Growth rates are 10-year compound averages.

A $1.3 million Sydney apartment yielding 2.9 per cent and a $520,000 Townsville house yielding 5.8 per cent are not just different price points. They represent different strategies. The Sydney asset may suit a growth-focused investor who can carry negative cash flow, while the Townsville asset may suit an investor who needs stronger income and less holding pressure.

Timing still matters, but less than many investors assume. Buyers who entered Sydney at points described as peak pricing in 2004 or 2017 often saw strong outcomes over the following decade.

That does not mean every entry point is safe. It means asset quality, holding period, and finance structure usually matter more than waiting for a perfect market.

Is Now a Good Time to Invest in Property in Australia?

Key factors include leading indicators in the Australian property market, whether now is a good time to invest, and assessing today’s property market conditions.

It can be, but only if the asset and finance structure are sound. A good time to invest is not defined by headlines. It is defined by whether the investor can buy a quality asset, hold it through stress, and stay invested long enough for the strategy to work.

For many investors, regional markets and smaller capitals now deserve more serious analysis. A higher-yielding property in a market with stable employment and rental demand may offer a better risk-adjusted fit than a more expensive capital city asset with weaker cash flow.

“Entry conditions matter. Entry decision quality matters more.”

What This Means in Practice

Investors should not begin with the question, “Where is the cheapest property?” They should begin with, “What kind of asset can my financial position safely support?”

That shift changes the search. It moves the investor away from broad market opinion and toward a clearer match between income, debt, cash flow, asset type, and time horizon.

Not sure what you can afford?

Find out exactly how much you can borrow and what it means for your next acquisition.

Property investment risks

A guide to property investment that does not address risk is not a complete guide. The following risks are not hypothetical. They appear regularly in investor portfolios and they are rarely discussed clearly before a purchase is made.

Interest Rate Risk

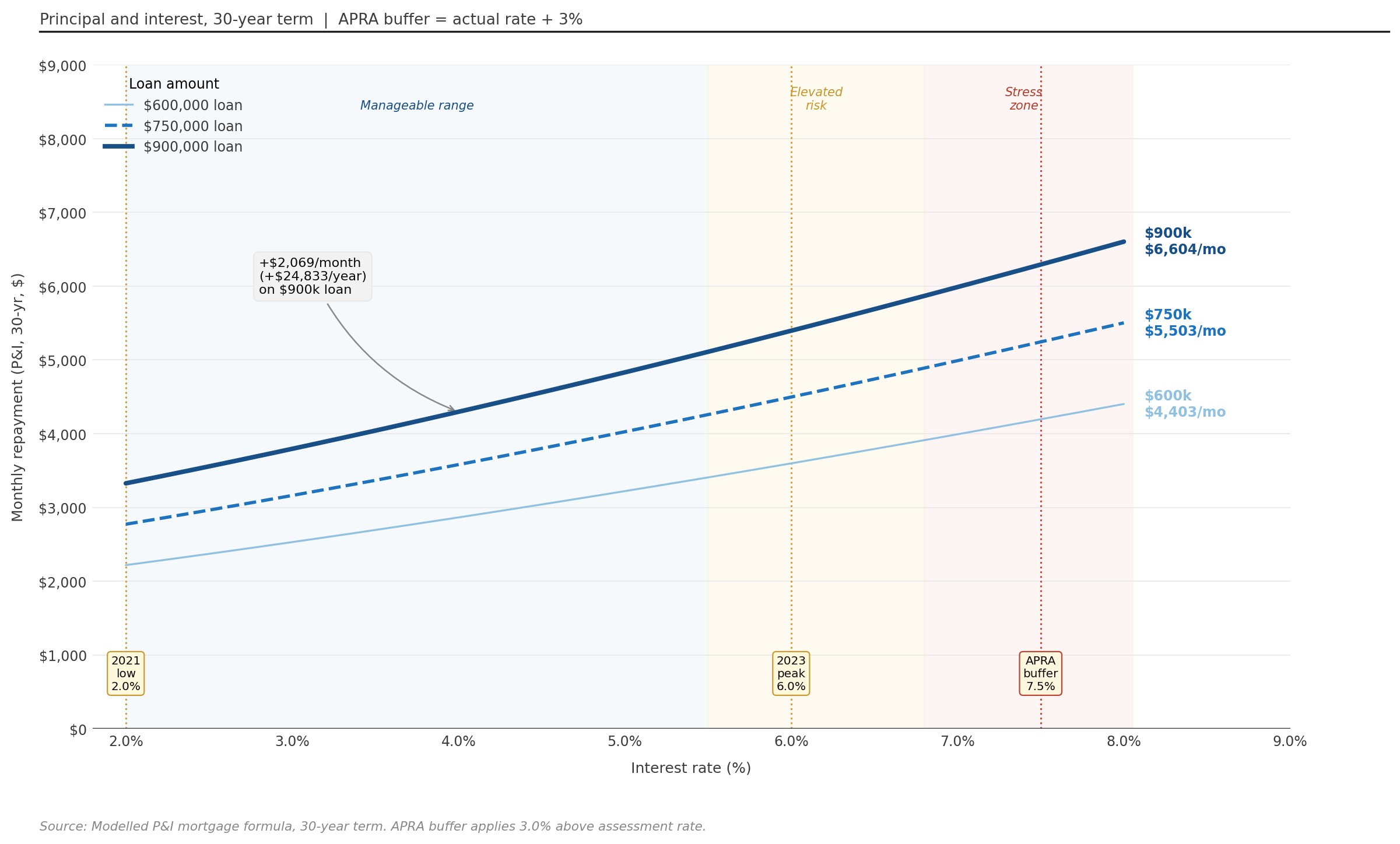

When rates rise, holding costs increase and serviceability deteriorates. A $900,000 loan at 2 per cent in 2021 cost roughly $3,300 per month in principal and interest. At 6 per cent, the same loan cost over $5,400. That $2,100 monthly difference is not a minor adjustment. It affects household cash flow, savings capacity, and the ability to buy again.

Many investors want to know how interest rates affect property investors, specifically the relationship between rates and property values and understanding interest rate impacts.

Stress testing every acquisition at a rate 2 to 3 per cent above the current level is not pessimism. It is basic discipline.

Vacancy Risk

A property without a tenant produces no income but continues to incur costs. Vacancy risk is highest in oversupplied markets, properties in weak rental demand areas, and premium segments where the pool of qualifying tenants is narrower.

Investors should model at least 2 to 4 weeks of vacancy per year in their holding cost calculations, and higher in more volatile markets.

Liquidity Risk

Property cannot be sold quickly without incurring significant cost or accepting a price reduction. If an investor needs to exit under pressure, the result is usually a below-market sale, stamp duty already paid, and selling costs that further reduce the net position.

This is one of the strongest arguments for maintaining adequate cash reserves and not stretching leverage to its maximum.

Borrowing Capacity Risk

Every acquisition affects the investor’s ability to borrow again. A portfolio that appears to be growing can quietly be consuming the borrowing capacity needed for future purchases. Lenders assess total debt exposure, debt-to-income ratios, and serviceability across the whole position.

Investors who have not modelled how each purchase affects future capacity often discover the constraint when they try to buy the second or third property.

Concentration Risk

A portfolio of three properties in the same suburb, same asset type, or same market segment is more exposed than a diversified one. If that market softens, the entire portfolio is affected simultaneously.

Geographic and asset-type diversification is not always possible in the early stages, but it should be a planning consideration as the portfolio grows.

Behavioural Risk

The risk that is least often discussed is the investor themselves. Panic selling at the bottom of a cycle, over-leveraging during a run-up, making emotional purchase decisions, or failing to plan the income transition toward retirement are all behavioural risks.

A strong investment plan does not only define what to buy. It defines what conditions would lead to a sale, how the investor will respond to market commentary, and what the decision-making process looks like under pressure.

“Risk is not only what happens in markets. It is also what happens in the investor’s mind when markets move against them.”

Want to Stress Test Your Current Position?

Our strategy team can model your portfolio against rate rises, vacancy, and borrowing constraints.

Common Property Investment Mistakes to Avoid

Most property investment mistakes are not dramatic. They are ordinary decisions made with incomplete information.

The damage often appears later, when the investor tries to refinance, buy the second property, or move toward retirement income.

Buying Based on Personal Preference

The most common first mistake is buying a property the investor likes rather than one the fundamentals support. A suburb can feel familiar and still be a weak investment market.

A good investment property should be assessed through demand, supply, land value, rental depth, employment access, transport, infrastructure, and comparable sales. Personal comfort should not lead the decision.

This is where many first-time investors confuse confidence with analysis.

Underestimating Holding Costs

Many investors model the mortgage and stop there. That is rarely enough.

Owning an investment property usually involves management fees, repairs, insurance, council rates, strata or body corporate costs where relevant, and vacancy. A property that looks neutral before those costs may create a real cash flow shortfall once they are included.

The gap between modelled cost and actual cost is where many first-year investors get their education.

Excessive Leverage Without Stress Testing

Leverage can build wealth, but only if the investor can stay solvent and calm while conditions change. A household with a $900,000 loan at 2 per cent in 2021 faced a very different repayment profile when rates moved toward 6 per cent.

For that size loan, the monthly repayment shift can be more than $2,000. That is not a small adjustment. It can change household behaviour, savings rates, and the ability to buy again.

Even a $600,000 loan enters elevated serviceability risk territory above the 2023 cycle peak. At the APRA stress buffer rate, all three loan sizes are well into pressure zones — which is precisely why lenders assess borrowers at a rate above the current offering, not the rate on the day of application.

Source: Modelled principal and interest mortgage formula, 30-year term, $900,000 loan. APRA lending data referenced for high debt-to-income lending trends.

The repayment shock from higher rates was not caused by poor property selection alone. It was often caused by finance structures that had not been tested against realistic rate increases. Stress testing is not pessimism. It is the basic discipline required when leverage is central to the strategy.

Stage-of-Life Mismatch

A 31-year-old and a 48-year-old can buy the same negatively geared property and be making completely different decisions. The younger investor may have time, income growth, and a long runway for capital growth. The older investor may need the portfolio to shift toward income within a decade.

Same asset. Different consequence.

This is why strategy must change with life stage. Growth assets can be useful early. They can become a problem later if the portfolio never converts toward income.

What Is the Biggest Mistake First-Time Property Investors Make?

The biggest mistake is buying with emotion before analysis. The second is underestimating the true cost of holding the property.

A first-time investor should run the full financial model before attending inspections, not after. That includes rent, vacancy, management fees, maintenance, insurance, rates, and higher interest rate scenarios.

“The investors who build sustained wealth are usually not the ones who buy the most exciting property. They are the ones who buy sound assets, hold through cycles, and avoid decisions that damage the next step.”

What This Means in Practice

Two properties can look similar online and produce very different outcomes. Small differences in location, tenant demand, land content, and holding cost can compound over time.

The discipline is simple: analyse first, inspect second, negotiate third. Reversing that order is how emotion enters the purchase.

How to Build Long-Term Wealth Through Property Investment

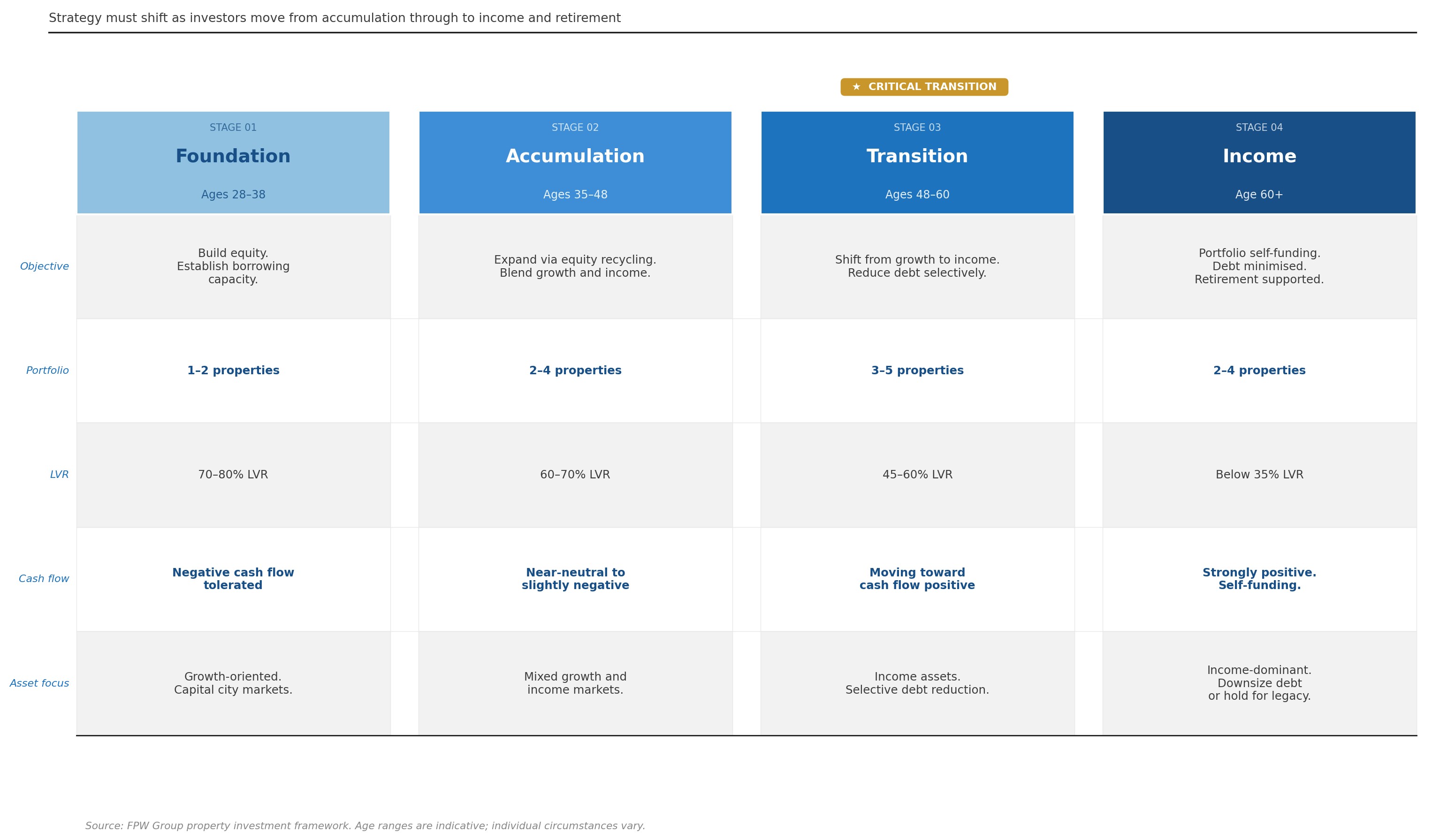

Long-term property wealth is usually built through a sequence, not a single purchase. The strategy changes as the investor moves from early accumulation toward income and retirement.

This is where many portfolios lose direction.

The critical transition between Accumulation and Transition stages is where most portfolios lose direction. Investors who do not deliberately shift their asset mix and debt strategy during their late 40s often arrive at retirement with strong equity but insufficient income to support the lifestyle they planned for.

Source: FPW Group property investment framework. Age ranges are indicative and individual circumstances vary.

Property strategy should shift from growth to income as the investor ages. Many investors reach their mid-50s with strong equity but weak cash flow. That is not a market failure. It is usually a sequencing failure.

Foundation Stage: Ages 28 to 38

In the foundation stage, the goal is usually to buy the first one or two investment properties and build equity. Growth-oriented assets can make sense because the investor has time and income growth ahead.

A 31-year-old accountant who buys a $480,000 townhouse and accepts a modest monthly shortfall may be making a rational trade. The aim is not immediate income. The aim is equity growth over the next decade.

Accumulation Stage: Ages 35 to 48

In the accumulation stage, the investor may use equity to expand the property portfolio. The focus begins to shift from pure growth toward a blend of growth and cash flow.

By this stage, the risk is often not the first property. It is the way the first property affects the next two decisions.

A strong portfolio is not just a set of good assets. It is a set of assets that work together.

Transition Stage: Ages 48 to 60

The transition stage is where the hardest decisions usually sit. The investor may have equity, but equity alone does not fund retirement.

A $2 million portfolio generating $40,000 a year in net rental income may not support the lifestyle the investor expects. Stated plainly, the arithmetic is obvious. Many investors only confront it too late.

This is the stage where debt reduction, asset sales, refinancing, and income-focused assets may need to be considered. Not because growth stops mattering, but because income begins to matter more.

Income and Retirement Stage: From Age 60

By retirement, the portfolio should ideally be easier to hold. Debt should be lower, income should be stronger, and the investment should support broader retirement planning.

This does not happen automatically. A growth portfolio does not quietly become an income portfolio because the investor turns 60.

It has to be planned earlier.

“The shift from equity growth to income generation is not automatic. It requires deliberate decisions about debt, asset mix, and timing.”

What This Means in Practice

Investors should start thinking about the transition to income well before retirement. Mid-40s is often a better planning window than late-50s.

By the time retirement is close, many of the structural decisions have already been made. The portfolio will either support flexibility, or it will force harder choices.

The Five Drivers of Property Investment Success

After working with hundreds of property investors, the outcomes that consistently separate strong portfolios from stalled ones come down to five things. Not market timing. Not suburb selection alone. Five structural factors that compound over time.

The Five Drivers of Property Investment Success

Asset Selection — Buying the right property in the right market for the right objective.

Borrowing Capacity — Managing the debt position so future acquisitions remain possible.

Cash Flow — Structuring the holding cost so the investor can stay in position through adversity.

Portfolio Sequencing — Ensuring each acquisition improves rather than limits the next.

Time — Staying invested long enough for compounding and capital growth to do their work.

Investors who are strong across all five tend to build wealth methodically. Investors who are weak on even one — particularly borrowing capacity or sequencing — often find the portfolio stalls despite strong individual asset choices.

How to Start Property Investing in Australia

The hardest part of starting is not usually interest. It is the number of decisions that arrive at once.

Price, deposit, loan structure, market selection, asset type, tax, rental demand, and future borrowing capacity all appear before the investor feels ready.

The way through is to put the decisions in the right order.

Start With Borrowing Capacity

A realistic borrowing capacity assessment should come before suburb research. The question is not only what a lender might approve today. It is what the investor can comfortably hold if rates rise, rent falls, or repairs arrive early.

A household earning $140,000 combined may technically qualify for a larger loan than it should take. A more conservative figure may leave room for vacancies, repairs, and future acquisitions.

In practice, many investors discover the borrowing constraint when they try to buy the second property. By then, the first loan may already have limited what comes next.

Investors who are strong across all five tend to build wealth methodically. Investors who are weak on even one — particularly borrowing capacity or sequencing — often find the portfolio stalls despite strong individual asset choices.

Know Your Numbers Before You Buy

A borrowing capacity assessment takes 30 minutes and changes how you approach the search.

Define the Investment Objective

An investor seeking long-term equity over 25 years needs a different asset from someone seeking income in eight years. The objective should be decided before engaging with listings, buyer’s agents, or advisers.

Without that clarity, the investor becomes easier to lead into a product-led recommendation. A strategy-led purchase starts with the outcome, then works backward to the asset.

Research Before Professional Engagement

A basic understanding of the target market improves the quality of advice. Investors do not need to become property analysts, but they should understand comparable sales, rent levels, vacancy pressure, infrastructure, and local employment drivers.

For a first acquisition, simplicity is often valuable. A well-located residential asset near employment and transport is usually easier to understand than a complex structure, development site, or off-the-plan contract.

Complexity can increase property investment risk, especially for investors still learning the asset class.

Commit to a Holding Period

Property has high entry and exit costs. Stamp duty, selling costs, and capital gains tax can reduce the benefit of short holding periods.

A property bought for $550,000 and sold for $700,000 after three years may produce a much smaller net result than the headline gain suggests. Held for 12 years, those same costs become less important relative to the total return.

How Much Deposit Do You Need to Invest in Property in Australia?

Most lenders require 10 to 20 per cent for investment properties. An 80 per cent loan-to-value ratio, meaning a 20 per cent deposit, is often the standard point where investors avoid Lenders Mortgage Insurance.

For a $650,000 property, that means about $130,000 in usable funds before transaction costs. Some investors use equity from an existing property instead of cash, but that increases total debt and can reduce future borrowing capacity.

“The first investment property does not need to be perfect. It needs to be financially sound, strategically useful, and affordable through more than one market condition.”

What This Means in Practice

Starting is not the hard part. Staying in is.

The investors who build wealth are usually the ones who can hold through downturns, refinance carefully, and let compounding work over 15 to 20 years. The decision to hold should be planned before pressure arrives.

Final Thoughts

Property investment in Australia has helped many households build wealth because it combines leverage, time, and a large real asset. None of that makes it automatic.

The environment is less forgiving than it was during the low-rate years. Borrowing capacity is tighter. Holding costs are higher. Entry prices in many markets have already moved.

That does not mean the opportunity has disappeared. It means the plan has to be sharper.

The strongest investors from here will not necessarily be the ones who find the cheapest property or the highest yield. They will be the ones who understand their stage of life, match the asset to the objective, model the debt honestly, and hold long enough for the strategy to work.

The fundamentals have not changed. The margin for poor planning has.

“Leverage, time, and compounding still work. What has changed is the level of discipline required to use them well.”

What This Means in Practice

This article covers the foundations. The real value sits in the detail: the market, the asset type, the lender, the holding cost, and the sequence of acquisitions.

If each purchase improves the next decision, the portfolio becomes stronger. If each purchase consumes borrowing capacity without improving the strategy, the portfolio eventually stalls.

Who we work with

Tailored strategy to guiding Australians at every stage of their property journey.

Frequently Asked Questions

1. Is Property Investment Still Worth It in Australia?

For investors with a clear strategy, sound financing, and a long enough time horizon, the answer is generally yes. The environment is more demanding than it was in the low-rate years. Borrowing capacity is tighter, entry prices are higher in many markets, and the margin for poor planning is smaller. But the fundamentals — leverage, compounding, and capital growth in supply-constrained markets — have not changed.

The better question is not whether property investment is worth it in the abstract. It is whether it is the right move for your specific financial position right now.

2. How Much Deposit Do I Need?

Most investment property lenders require between 10 and 20 per cent. At 80 per cent loan-to-value, a $650,000 property requires roughly $130,000 in usable equity or cash before accounting for stamp duty and transaction costs. Some investors access equity from an existing property, but this increases total debt and affects serviceability calculations.

3. House or Apartment?

Both can perform well depending on market and strategy. Houses tend to have higher land content and historically stronger capital growth in metropolitan areas. Apartments can offer higher yields and lower entry prices, but come with body corporate fees, strata levies, and in some markets, higher supply risk.

The more useful question is not house versus apartment. It is which asset type in which market best matches your objective and borrowing position.

4. Growth or Cash Flow?

This depends on life stage. Younger investors with time and income can often accept the cash flow drag of a growth-oriented asset. Investors closer to retirement typically need the portfolio to generate more income.

A blended strategy that targets reasonable growth with manageable cash flow is often the most practical approach for investors in their late 30s and 40s.

5. How Many Properties Should I Own?

There is no universal target. Some investors build wealth with two well-chosen properties over 20 years. Others build portfolios of five or more. The limit is usually borrowing capacity, not ambition.

A more useful goal than a property count is this: each acquisition should leave the investor in a better financial position, with more options rather than fewer. If the next purchase limits future borrowing capacity more than it builds equity, the sequencing needs to be reconsidered.

Ready to Build Your Property Investment Strategy?

Book a strategy call with the FPW team. We’ll map your borrowing capacity, review your current position, and help you plan the next acquisition with confidence.

© Copyright 2026. FPW. All Rights Reserved.